Table of Contents

Our Global Presence :

Home / Blog / Blockchain

Credit Card Tokenization: Safeguarding Data in a Digital Era

by

December 24, 2024

by

December 24, 2024

Credit card tokenization is changing the payment processing industry by providing an innovative approach to protect sensitive data during online transactions.

As online shopping and the use of digital payments are increasing, so is the risk of data breaches and identity theft. In the US alone, credit card fraud accounts for nearly half of all identity theft reports in the US, totalling 1,036,903 cases. Not just this, 44% of credit cardholders reported experiencing fraudulent charges two or more times in 2022, up from 35% in 2021.

Tokenization addresses these problems by replacing sensitive credit card information with unique identifiers so that if data is ever hacked, it can’t be misused by bad actors.

In this article, we will cover the definition of credit card tokenization, how it works and its benefits. We will also discuss steps for tokenizing your credit card, as well as its real-world applications and challenges and solutions associated with credit card tokenization.

What is Credit Card Tokenization?

Credit card tokenization is a security process that replaces sensitive credit card information—such as the primary account number (PAN)—with a unique, randomly generated string of characters, known as a token. The token itself holds no meaningful value and cannot be reverse-engineered to retrieve the original data. This technique ensures that sensitive cardholder information is never stored in vulnerable environments, minimizing exposure during payment processes.

Unlike encryption, which transforms data into a coded format, tokenization removes sensitive data entirely from the ecosystem, making it one of the most secure methods for protecting payment information.

Time to Embrace Tokenization? Let’s Make It Work for You!

Protecting data doesn’t have to be a hassle. With tokenization, you can boost security and customer trust without breaking a sweat. Let’s join forces to bring this cutting-edge solution to your payment systems.

How Does Credit Card Tokenization Work?

Credit card tokenization involves several steps to secure payment transactions; they are:

1. Customer Initiates Payment: The customer provides their credit card details for a purchase.

2. Data Transmission: The credit card details are sent to a tokenization service provider.

3. Token Generation: This is part of the token development phase. The provider generates a random, unique token to replace the sensitive information.

4. Token Storage: The token is sent back to the merchant and stored in their system, while the original card data is securely stored in the provider’s token vault.

5. Transaction Processing: During subsequent transactions, the token is used instead of the actual card details, ensuring sensitive information never re-enters the merchant’s system.

6. Token Validation: The token is mapped back to the original data by the provider for transaction authorization.

Credit Card Tokenization vs. Encryption

Though both tokenization and encryption share the same goals – namely, to protect sensitive data, but they have different methodologies and applications. Knowing the differences will enable you to choose the right security strategy for your business.

Tokenization Explained

In tokenization, the sensitive credit card information, such as the PAN, is replaced with a randomly generated token. This token has no inherent value, and it is not possible to reverse it to retrieve the original information. The original sensitive information is stored securely in a centralized token vault managed by the tokenization service provider.

Key characteristics of tokenization include:

- Irreversibility: Tokens are meaningless outside the token vault, making them useless to unauthorized users.

- Minimal Data Exposure: Sensitive data never resides in the merchant’s system, reducing vulnerability to breaches.

- Specific Use Case: Tokens are unique to each transaction or merchant, ensuring they cannot be reused elsewhere.

Related Read: What is Tokenization

Encryption Explained

On the other hand, encryption converts sensitive data into a coded format using an encryption algorithm and a cryptographic key. Only the matching key can decrypt the encrypted data, so only those with the correct key have access to the original information.

Key characteristics of encryption include:

- Reversibility: Encrypted data can be reverted to its original form if the decryption key is compromised.

- Data Retention: The original data remains in the system but is stored in an unreadable format.

- Versatility: Encryption can be applied to a wide range of data, not just payment information.

Differences Between Tokenization and Encryption

Here are the differences between tokenization and encryption:

1. Security Approach

Data tokenization removes sensitive data entirely, replacing it with tokens that have no intrinsic value. This makes it particularly effective for payment systems where minimizing data exposure is critical.

Encryption secures data by transforming it into an unreadable format. While effective, it retains the original data in the ecosystem, requiring robust key management practices.

2. Reversibility

Tokenization is inherently irreversible without access to the secure token vault.

Encryption relies on keys, making it vulnerable if the key management system is compromised.

3. Compliance

Tokenization simplifies compliance with Payment Card Industry Data Security Standards (PCI DSS) by reducing the scope of sensitive data stored within a system.

Encryption requires additional safeguards to meet PCI DSS requirements, as the encrypted data is still considered sensitive.

4. Data Usage

Tokens are tailored for specific use cases, such as a particular merchant or transaction, reducing their applicability outside their intended context.

Encrypted data can be used across multiple applications, provided the decryption key is accessible.

5. Integration

Tokenization often requires integration with a tokenization provider’s systems and APIs, making it reliant on external services.

Encryption is typically implemented internally, giving businesses more control but also requiring significant technical expertise.

Both techniques are important in payment systems security, and companies might use a combination of AI tokenization and encryption for the best protection given their own needs. Tokenization is often the technology of choice for protecting credit card information, particularly as it can extract sensitive data from the environment completely.

The Benefits of Credit Card Tokenization

Tokenization offers several advantages that make it indispensable for secure transactions:

1. Enhanced Security

Tokenization takes sensitive information and replaces it with a unique identifying string so that during a data breach, nothing valuable is accessible. This reduces the exposure to identity theft and fraud, ensuring strong protection against any instances of cardholder data being accessed without authorization. Tokenization platforms function as an essential defense mechanism in online transactions.

2. Seamless Transactions

Tokenizing also facilitates secure and efficient payment processing without disrupting the customer experience. As sensitive data is switched for tokens, businesses can streamline transactions, cut the processing time in half, and maintain consistency as well. This seamless combination improves operational efficiency and ensures reliable security for online and in-store payment systems.

3. PCI Compliance

Tokenization streamlines compliance with Payment Card Industry Data Standards (PCI DSS) by getting rid of sensitive card data from a merchant’s environment. In other words, it reduces PCI DSS compliance requirements.

Having less strict security requirements to fulfill allows businesses to put their mind at ease and concentrate on their core operations, while still being able to rely on a secure payment infrastructure that fits industry regulations and safeguards both its customer trust and sensitive information.

4. Reduced Liability

In case of security breaches, businesses are significantly less liable because they offload the responsibility of storing and managing sensitive data to a tokenization provider. As the tokenized credit card data is impossible to trace back to the original credit card data, this helps to ease fears about reputational damage and potential legal issues faced due to data leaks.

5. Customer Trust

Tokenization adoption shows a company’s commitment to protecting customer data. Customers are more likely to repeat a transaction when they are confident that their payment information is secure, creating loyalty and improving brand reputation.

Tokenization acts as a trust-building measure in an increasingly security-conscious marketplace.

6. Cost savings

Investing in tokenization reduces the financial impact of potential data breaches, such as high fines, legal fees, and remediation expenses. Furthermore, simplifying PCI DSS compliance will save businesses money on audits and infrastructure upgrades. In the long run, tokenization proves to be cost-effective, especially for organizations with high transactional volume. Even if an organization decides to tokenize their real-world assets, they need to partner with a reputable real estate tokenization company to enjoy these benefits.

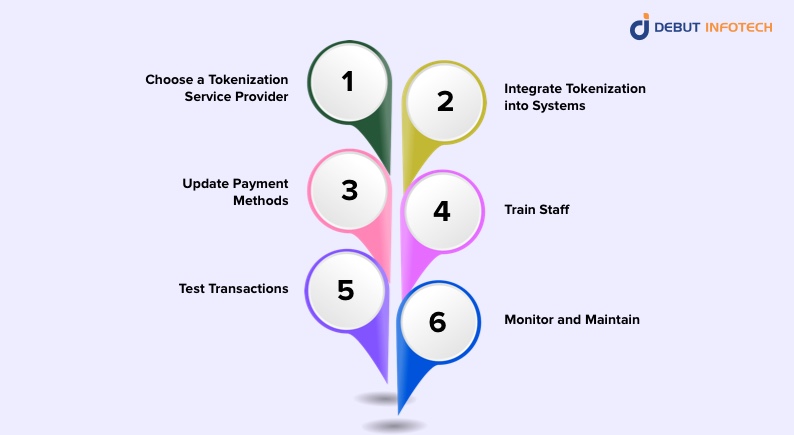

Steps for Tokenizing Your Credit Card

To integrate tokenization into your payment processes, follow these six steps:

1. Choose a Tokenization Service Provider

This is the first step in the credit card tokenization process. So, choose a reputable provider with robust security protocols, industry certifications, and a good track record. Look for those that specialize in tokenizing payment where they need to work with regulatory compliance like PCI DSS to ensure your transactions are secure.

2. Integrate Tokenization into Systems

With guidance from your provider, integrate their APIs or software onto your payment platforms. This could be your e-commerce site, mobile app, or POS system to ensure that all transactions are tokenized seamlessly.

3. Update Payment Methods

Replace existing processes that store sensitive card data with token-based storage. Coordinate with your provider to securely migrate stored data into tokens, ensuring continuity in processing payments without compromising security.

4. Train Staff

Educate your team on tokenization practices, including how it works and why it’s crucial. Make sure they understand their role in maintaining a secure payment environment and addressing customer questions confidently.

5. Test Transactions

Run extensive tests on your payment system to ensure tokens are being generated, stored, and used correctly. Check for any errors in credit card processing tokenization and verify that all transactions remain smooth for customers.

6. Monitor and Maintain

Regularly review your tokenization system for performance, security updates, and compliance requirements. Stay in touch with your provider for support and adapt to new technologies or regulations to maintain a secure setup.

Real-World Applications of Credit Card Tokenization

Tokenization is widely used across various industries:

1. E-commerce Platforms

Online stores use tokenization to protect saved card information for future purchases. This means that instead of storing the actual card number, they store a token, keeping customer data safe in the event the platform is hacked. This builds trust and minimizes the risk of data breaches; therefore, customers can shop in a secure virtual environment.

2. Mobile Payment Apps

During transactions, apps like Apple Pay and Google Pay tokenize card information. That’s why when you tap to pay, the merchant doesn’t get your actual card information, but only a token. This provides an additional layer of security, which makes mobile payment solutions more secure and reliable for both consumers and businesses.

3. Point of Sale Retail Systems

In brick-and-mortar stores with up-to-date POS systems, tokenization helps to keep your card details safe during in-store transactions. When the card is swiped or tapped, a token is created. Since the token does not reveal the credit card data, the system doesn’t store the information of the actual card data. This means that malware or system breaches cannot compromise your card information.

4. Travel and Hospitality Industry

Hotels and airlines use payment tokenization to secure payment details for bookings, deposits, and rewards programs. By replacing card data with tokens, they safeguard customer information while streamlining operations like reservations and check-ins, creating a secure and convenient experience for travelers.

5. Subscription Services

For streaming services, fitness apps, or other subscription-based businesses, tokenization helps them process recurring payments without storing sensitive credit card data. In the long run, this reduces liability and ensures uninterrupted service for customers while maintaining strict security standards.

Credit Card Tokenization Challenges & Solutions

While tokenization is effective, it comes with certain challenges:

1. Integration with Legacy Systems

Older systems in businesses may not support tokenization even real world asset tokenization, making integration difficult. This can lead to compatibility issues, operational delays, or expensive upgrades. Many organizations face challenges adapting their infrastructure to work seamlessly with modern tokenization technologies.

Solution: Collaborate with experienced tokenization providers who offer integration support. They can customize solutions to bridge the gap between legacy systems and tokenization, minimizing disruptions. Gradually upgrading systems to newer, more compatible technologies also ensures long-term efficiency.

2. Dependency on Third-Party Providers

Relying on tokenization service providers also carries the risk of service interruptions, or vendor-specific limitations.

Suppose the provider’s systems go down, or experience downtimes. In that case, businesses may face transaction delays or disruptions, which will affect customer satisfaction and revenue.

Solution: Choose a reliable provider with a robust service-level agreement (SLA) and proven uptime track record. Implement fallback measures like redundant systems or multiple providers to reduce dependency and ensure continuity during unforeseen issues.

3. Token Vault Security Risks

While tokens are safe, the token vault storing the original card data becomes a critical vulnerability. A breach of this centralized repository can lead to significant data exposure, undermining the purpose of tokenization.

Solution: Select providers with advanced security measures, including encryption, access controls, and regular audits, for their token vaults. Employ multi-factor authentication and real-time monitoring to detect and address potential threats promptly, enhancing the overall security framework.

4. Performance Overhead

For businesses with high throughput, tokenization can also cause some delays in transaction processing. Communication with the tokenization provider is required for each token request and validation, which may negatively impact system performance and create slower experiences for customers.

Solution: Engage with a provider that provides low-latency solutions & scalable systems to optimize integration. Furthermore, consider caching commonly used tokens and routinely auditing the system performance to detect any chokepoints. Focus on robust infrastructure upgrades to ensure the system can handle increased speed without sacrificing security.

Conclusion

Credit card tokenization has become a pillar of security for digital payments. It can help mitigate fraud and ensure compliance with regulatory requirements by replacing sensitive card data with secure tokens.

With tokenization, businesses stand to gain increased security, decreased liability, and improved customer trust. This sets them up for long-term success in an increasingly digital world. Adopting this secure approach is no longer a best practice but a requirement in the modern payment ecosystem.

FAQs

Q. How do I tokenize my credit card number?

To tokenize your credit card, you usually don’t have to do much yourself. When you make a payment through a secure payment gateway or use a digital wallet like Apple Pay, your card details are automatically tokenized. Just make sure the service or merchant you’re using supports tokenization.

Q. What is an example of credit card tokenization?

Imagine you save your card for future use on a shopping app. Instead of storing your actual card number, the app replaces it with a random token like “ABC123XYZ.” This token is useless outside that system. So, even if hackers get it, they can’t steal your money.

Q. How to remove credit card tokenization?

Removing tokenization is straightforward—just delete your saved card details from the app or platform storing them. The token gets invalidated automatically. If you’re using a digital wallet, you can remove the card from your account, and its associated token is wiped.

Q. How much does tokenization cost?

Tokenization costs vary, but many payment processors bundle it into their services at no extra charge. Some might charge a small fee, depending on the transaction volume or the provider. Either way, the added security is worth it for businesses and customers alike.

Q. What is the problem with credit card tokenization?

The main issue is dependency on third-party tokenization providers. If their system goes down or the token vault is compromised, transactions can halt. Plus, integrating tokenization into some older systems can be a bit of a headache, but it’s usually a one-time challenge.

Talk With Our Expert

Our Latest Insights

USA

Debut Infotech Global Services LLC

2102 Linden LN, Palatine, IL 60067

+1-703-537-5009

info@debutinfotech.com

UK

Debut Infotech Pvt Ltd

7 Pound Close, Yarnton, Oxfordshire, OX51QG

+44-770-304-0079

info@debutinfotech.com

Canada

Debut Infotech Pvt Ltd

326 Parkvale Drive, Kitchener, ON N2R1Y7

+1-703-537-5009

info@debutinfotech.com

INDIA

Debut Infotech Pvt Ltd

C-204, Ground floor, Industrial Area Phase 8B, Mohali, PB 160055

9888402396

info@debutinfotech.com

Copyright © 2025, Debut Infotech. All rights reserved. | Privacy Policy

Leave a Comment